Top P2P lending Platforms and Apps in India

Prashanth Kancherla

Feb 24, 2026 | 9 mins read

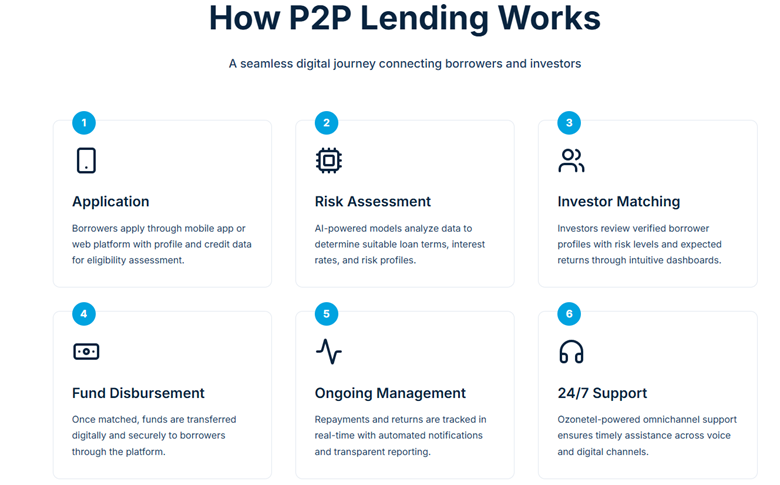

P2P Lending Process Explained

Let’s take a quick look at the key steps involved in peer-to-peer lending process in India.

Top 10 P2P Lending Platforms

Now that you have a good understanding of what peer-to peer lending is and how it works, here are some of the top 10 P2P lending companies that you can opt for:

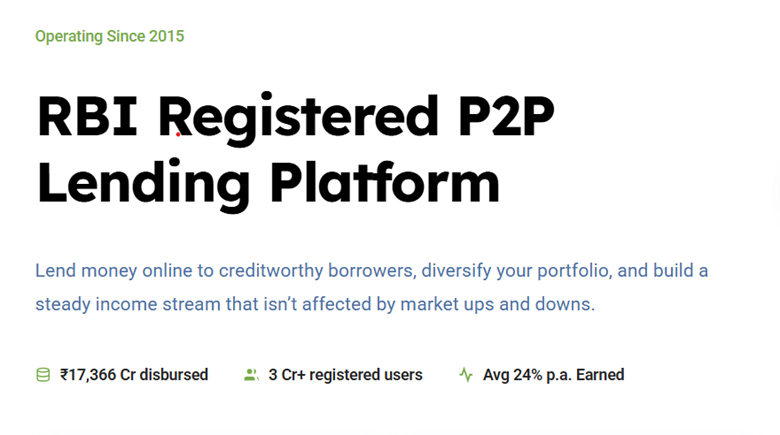

LenDenClub

LenDenClub is a RBI-registered peer-to-peer lending platform with a wide retail investor base and strong loan disbursement history. The platform offers multiple loan types (personal, business, medical) and operates fully online. So far, the platform has disbursed over ₹17,366 crore in loans and has over 3 crore registered users.

Key Features

- Loan tenures range from 1 month to 36 months

- Zero withdrawal fees on invested funds

- Options for monthly payouts or auto-reinvestment

- Platform fees range between 0% and 4% of the amount lent

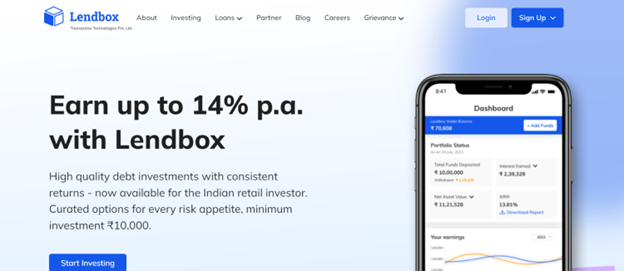

Lendbox

Lendbox is licensed by the Reserve Bank of India under the NBFC-P2P model. It focuses on high-quality borrower profiles and a user-friendly dashboard, making it a preferred choice for retail investors.

Key Features

- Loan tenures range from 1 month to 36 months

- Interest earned through borrower repayments

- Platform fees range between 0%–4% of amount lent

- Flexible investment options enabling diversification

- Focus on verified, creditworthy borrowers

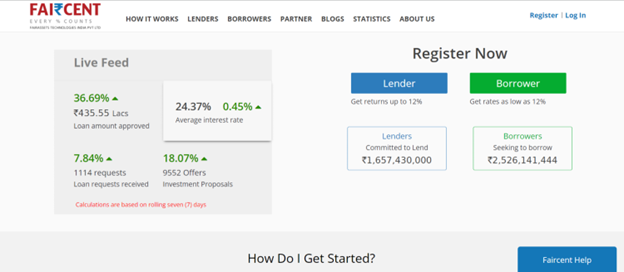

FairCent

Faircent is one of India’s earliest RBI-registered NBFC-P2P platforms which offers multiple loan categories for borrowers and diversified investment opportunities for lenders. The platform is suitable for both suitable for both short-term and longer-term financing needs.

Key Features

- Loan categories include personal, business, marriage, and property-backed

- Loan tenures range from 6 to 36 months

- 100% online process, no physical documentation

- Zero collateral loans for eligible borrowers

- Web and mobile app access available

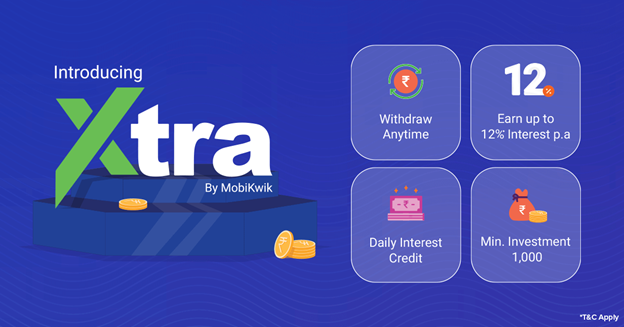

MobikwikXtra

Mobikwik Xtra is a P2P-backed investing feature within the Mobikwik app that enables users to earn returns on micro-lending investments. An investment as small as ₹10,000 can be distributed across more than 100 borrowers, helping investors diversify risk,

Key Features

- Access to detailed borrower profiles

- Loan tenure from 3 months to 2 years

- Suitable for small-ticket investors

- Integrated within Mobikwik app

- provides up to 14% returns per annum

IndiaP2P

IndiaP2P is an RBI-certified NBFC-P2P platform offering diversified lending plans, including monthly income options for investors. India P2P provides advanced security measures for safe and secure transactions.

Key Features

- Minimum investment typically starts from ₹10,000

- Multiple investment plans with diversified risk exposure

- Provides monthly payouts

- Lenders can earn up to 18% per annum

- Loan tenures up to 36 months

- Secure digital onboarding and monitoring

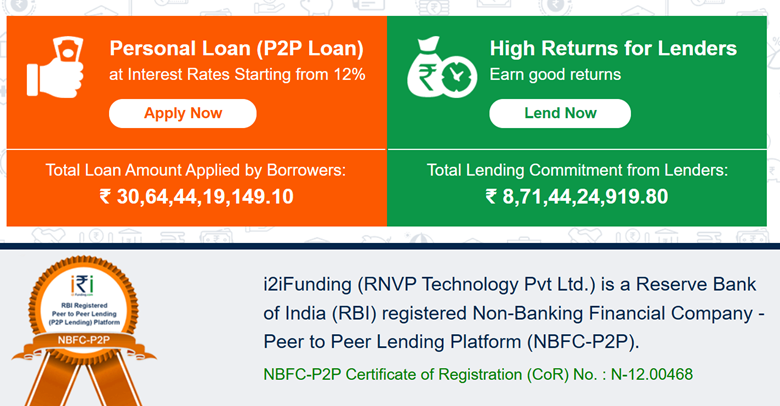

I2iFunding

i2i Funding is an online peer-to-peer lending platform that focuses on small-ticket, short-tenure loans designed for borrowers with a higher likelihood of repayment. The platform supports unsecured personal, business, and specific consumer-purpose loans.

Key Features

- Small-ticket loans starting from ₹1,000 to ₹5,000 per loan

- Short-tenure lending focused on faster repayment cycles

- In-house underwriting team for detailed credit assessment

- Physical verification conducted for select borrower profiles

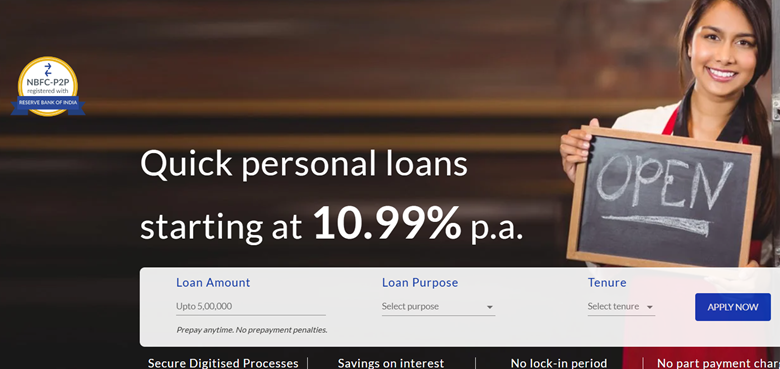

Finzy

Finzy is a regulated P2P lending platform offering simplified personal loan products with a borrower-friendly experience. The platform makes the entire borrowing process simple and user friendly. Borrowers can avail loan in as little as 48 hours

Key Features

- Offers loans from ₹50,000 to ₹5 Lakh

- Rigorous credit assessment process

- Loan tenures range from 6 to 24 months

- Automated repayment tracking

- risk-based pricing system for the borrowers

CRED Mint

CRED Mint is an investment offering integrated within the CRED ecosystem, developed in partnership with Liquiloans. It enables CRED members to participate in peer-to-peer style lending through a curated and regulated structure.

Key Features

- Investment range from ₹1 lakh to ₹50 lakh

- Daily portfolio tracking directly within the CRED app

- Curated borrower selection through a regulated lending structure

- Returns of up to 9% per annum

- Emphasis on lower-risk profiles

RupeeCircle

RupeeCircle is an RBI-registered NBFC-P2P lending platform that directly connects borrowers with investors through a technology-driven marketplace. The platform has over 306,000 registered users, including 86,000+ active investors.

Key Features

- Minimum investment starts from ₹5,000, across single or multiple loans

- Proprietary credit scoring model assigns risk grades and interest rates

- Focus on unsecured personal loans

- Flexible repayment schedules with loan tenures up to 36 months

- End-to-end digital borrower risk assessment

RangDe

RangDe is India’s first peer-to-peer social investment platform, focused on expanding access to credit for underserved rural entrepreneurs. It enables individuals to lend directly to farmers, artisans, and small business owners, helping build sustainable livelihoods while delivering meaningful, impact-led returns.

Key Features

- Minimum investment starts from ₹500

- Focus on micro-loans for underserved and rural communities

- Longer-term lending designed for sustainable livelihood impact

- Transparent borrower stories and clearly defined use cases

- Strong emphasis on social returns over high financial yields

Top P2P lending Platforms and Apps in India

Prashanth Kancherla

Feb 24, 2026 | 9 mins read

P2P Lending Process Explained

Let’s take a quick look at the key steps involved in peer-to-peer lending process in India.

Top 10 P2P Lending Platforms

Now that you have a good understanding of what peer-to peer lending is and how it works, here are some of the top 10 P2P lending companies that you can opt for:

LenDenClub

LenDenClub is a RBI-registered peer-to-peer lending platform with a wide retail investor base and strong loan disbursement history. The platform offers multiple loan types (personal, business, medical) and operates fully online. So far, the platform has disbursed over ₹17,366 crore in loans and has over 3 crore registered users.

Key Features

- Loan tenures range from 1 month to 36 months

- Zero withdrawal fees on invested funds

- Options for monthly payouts or auto-reinvestment

- Platform fees range between 0% and 4% of the amount lent

Lendbox

Lendbox is licensed by the Reserve Bank of India under the NBFC-P2P model. It focuses on high-quality borrower profiles and a user-friendly dashboard, making it a preferred choice for retail investors.

Key Features

- Loan tenures range from 1 month to 36 months

- Interest earned through borrower repayments

- Platform fees range between 0%–4% of amount lent

- Flexible investment options enabling diversification

- Focus on verified, creditworthy borrowers

FairCent

Faircent is one of India’s earliest RBI-registered NBFC-P2P platforms which offers multiple loan categories for borrowers and diversified investment opportunities for lenders. The platform is suitable for both suitable for both short-term and longer-term financing needs.

Key Features

- Loan categories include personal, business, marriage, and property-backed

- Loan tenures range from 6 to 36 months

- 100% online process, no physical documentation

- Zero collateral loans for eligible borrowers

- Web and mobile app access available

MobikwikXtra

Mobikwik Xtra is a P2P-backed investing feature within the Mobikwik app that enables users to earn returns on micro-lending investments. An investment as small as ₹10,000 can be distributed across more than 100 borrowers, helping investors diversify risk,

Key Features

- Access to detailed borrower profiles

- Loan tenure from 3 months to 2 years

- Suitable for small-ticket investors

- Integrated within Mobikwik app

- provides up to 14% returns per annum

IndiaP2P

IndiaP2P is an RBI-certified NBFC-P2P platform offering diversified lending plans, including monthly income options for investors. India P2P provides advanced security measures for safe and secure transactions.

Key Features

- Minimum investment typically starts from ₹10,000

- Multiple investment plans with diversified risk exposure

- Provides monthly payouts

- Lenders can earn up to 18% per annum

- Loan tenures up to 36 months

- Secure digital onboarding and monitoring

I2iFunding

i2i Funding is an online peer-to-peer lending platform that focuses on small-ticket, short-tenure loans designed for borrowers with a higher likelihood of repayment. The platform supports unsecured personal, business, and specific consumer-purpose loans.

Key Features

- Small-ticket loans starting from ₹1,000 to ₹5,000 per loan

- Short-tenure lending focused on faster repayment cycles

- In-house underwriting team for detailed credit assessment

- Physical verification conducted for select borrower profiles

Finzy

Finzy is a regulated P2P lending platform offering simplified personal loan products with a borrower-friendly experience. The platform makes the entire borrowing process simple and user friendly. Borrowers can avail loan in as little as 48 hours

Key Features

- Offers loans from ₹50,000 to ₹5 Lakh

- Rigorous credit assessment process

- Loan tenures range from 6 to 24 months

- Automated repayment tracking

- risk-based pricing system for the borrowers

CRED Mint

CRED Mint is an investment offering integrated within the CRED ecosystem, developed in partnership with Liquiloans. It enables CRED members to participate in peer-to-peer style lending through a curated and regulated structure.

Key Features

- Investment range from ₹1 lakh to ₹50 lakh

- Daily portfolio tracking directly within the CRED app

- Curated borrower selection through a regulated lending structure

- Returns of up to 9% per annum

- Emphasis on lower-risk profiles

RupeeCircle

RupeeCircle is an RBI-registered NBFC-P2P lending platform that directly connects borrowers with investors through a technology-driven marketplace. The platform has over 306,000 registered users, including 86,000+ active investors.

Key Features

- Minimum investment starts from ₹5,000, across single or multiple loans

- Proprietary credit scoring model assigns risk grades and interest rates

- Focus on unsecured personal loans

- Flexible repayment schedules with loan tenures up to 36 months

- End-to-end digital borrower risk assessment

RangDe

RangDe is India’s first peer-to-peer social investment platform, focused on expanding access to credit for underserved rural entrepreneurs. It enables individuals to lend directly to farmers, artisans, and small business owners, helping build sustainable livelihoods while delivering meaningful, impact-led returns.

Key Features

- Minimum investment starts from ₹500

- Focus on micro-loans for underserved and rural communities

- Longer-term lending designed for sustainable livelihood impact

- Transparent borrower stories and clearly defined use cases

- Strong emphasis on social returns over high financial yields

Ozonetel Live

Upcoming Webinar

Make it easy for your customers to reach you wherever, whenever, or to help themselves through bots pre-trained to solve retail use cases.

Learn more

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate

Description, experiences: Curating communicative & collaborative customer journeys in Real Estate